ABA Vs Routing Number: Understanding The Differences And Importance

ABA vs Routing Number has become a significant topic for individuals and businesses dealing with banking transactions. Whether you're transferring funds domestically or internationally, understanding these terms is crucial. The ABA routing number plays a pivotal role in ensuring that your money reaches the intended recipient without delays. In this article, we will delve into the differences between ABA and routing numbers, their functions, and why they matter in today's banking ecosystem.

The financial world relies heavily on accurate and secure processes to handle transactions. ABA routing numbers are an integral part of this system, ensuring that banks and financial institutions can communicate efficiently. This article will provide a comprehensive guide to understanding ABA vs routing numbers, their purposes, and how they differ from one another.

As you navigate through this article, we will explore the history, functionality, and applications of ABA routing numbers. By the end, you will have a clear understanding of why these numbers are essential and how they contribute to the smooth operation of financial transactions. Let's dive in.

Read also:How To Connect To Raspberry Pi Via Internet A Comprehensive Guide

Table of Contents

- ABA vs Routing Number

- What is an ABA Routing Number?

- History of ABA Routing Numbers

- Types of Routing Numbers

- Differences Between ABA and Routing Numbers

- Functions of Routing Numbers

- Finding Your Routing Number

- Security and Privacy Concerns

- Common Questions About ABA vs Routing Numbers

- Conclusion

ABA vs Routing Number: An Overview

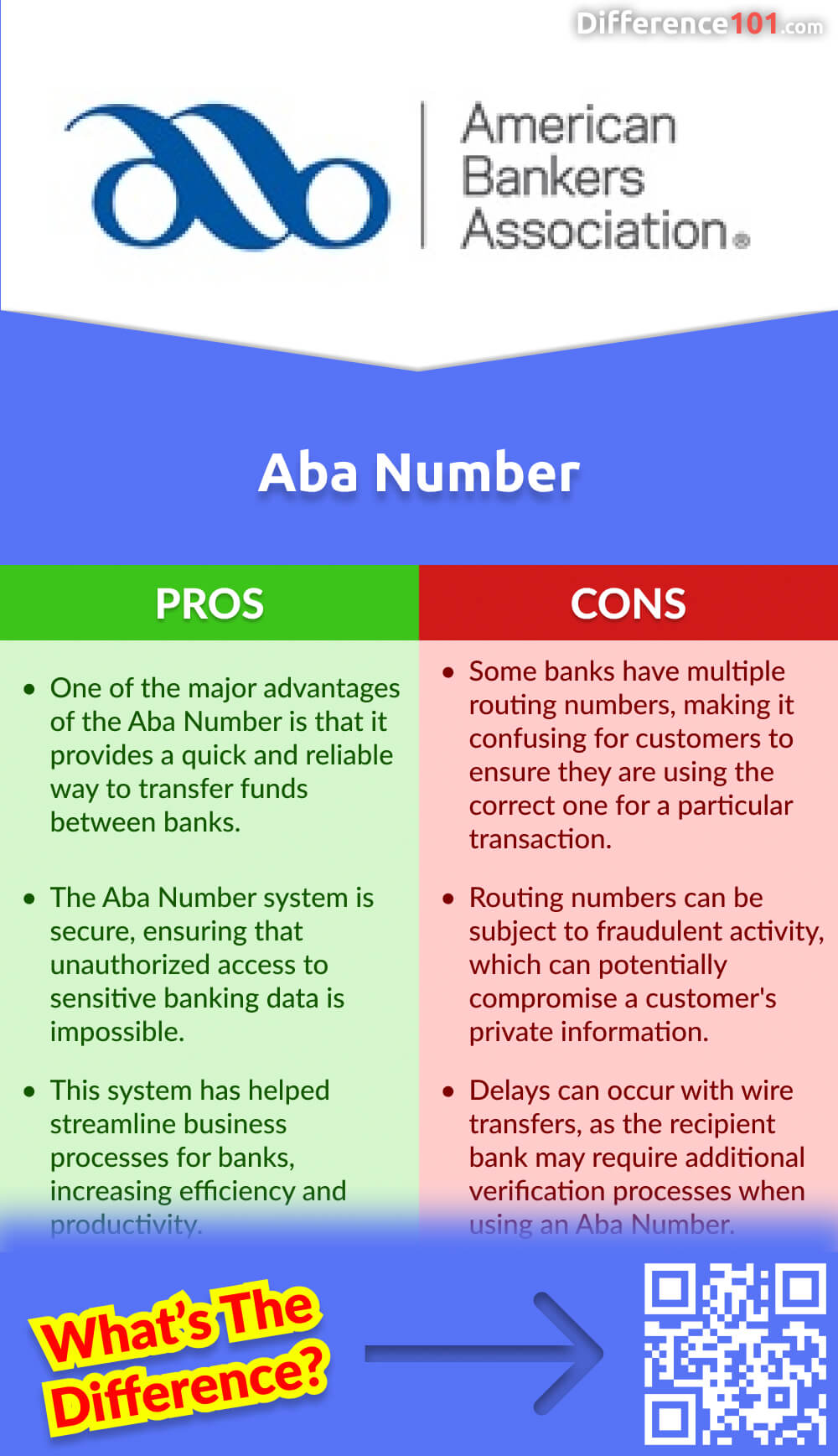

The terms "ABA" and "routing number" are often used interchangeably, but they refer to the same concept. ABA stands for the American Bankers Association, which developed the routing number system in 1910. The routing number is a nine-digit code used to identify financial institutions in the United States. It ensures that funds are routed to the correct bank or credit union during transactions.

When discussing ABA vs routing number, it's important to note that the ABA routing number is the official term used by financial institutions. This number is crucial for various banking activities, including direct deposits, bill payments, and wire transfers. Understanding the nuances of these terms will help you navigate banking processes more effectively.

What is an ABA Routing Number?

An ABA routing number is a unique nine-digit code assigned to financial institutions in the United States. It serves as a digital address that helps banks and credit unions identify where funds should be sent. The routing number is essential for processing checks, electronic transfers, and other financial transactions.

Structure of an ABA Routing Number

The ABA routing number consists of three components:

- Four digits representing the Federal Reserve Routing Symbol

- Four digits identifying the bank or financial institution

- One check digit used to validate the routing number

This structure ensures that each routing number is unique and can be verified easily.

History of ABA Routing Numbers

The ABA routing number system was introduced in 1910 by the American Bankers Association to streamline check processing. Initially, the system was designed to handle paper checks, but it has evolved to accommodate electronic transactions as well. Over the years, the routing number system has become an integral part of the U.S. banking infrastructure.

Read also:St Jude Valentines Day Card A Heartfelt Way To Spread Love And Hope

Today, the routing number system is managed by Accuity, a global provider of financial data and software solutions. Accuity ensures that routing numbers remain up-to-date and accurate, helping financial institutions maintain efficient operations.

Types of Routing Numbers

There are two main types of routing numbers:

1. ACH Routing Numbers

ACH (Automated Clearing House) routing numbers are used for electronic transactions, such as direct deposits and bill payments. These numbers are typically the same as the standard routing number for most banks, but some institutions may have separate ACH routing numbers.

2. Wire Transfer Routing Numbers

Wire transfer routing numbers are used for domestic and international wire transfers. These numbers are often different from standard routing numbers and are required for high-value transactions.

Understanding the differences between these types of routing numbers is essential for ensuring that your transactions are processed correctly.

Differences Between ABA and Routing Numbers

While the terms "ABA" and "routing number" are often used interchangeably, there are subtle differences between them:

- ABA Routing Number: The official term used by financial institutions to describe the nine-digit code.

- Routing Number: A more general term that refers to the same nine-digit code.

These differences are primarily semantic, but it's important to use the correct terminology when discussing banking processes.

Functions of Routing Numbers

Routing numbers serve several important functions in the banking system:

- Identifying financial institutions

- Facilitating check processing

- Enabling electronic transfers

- Supporting wire transfers

By providing a unique identifier for each bank or credit union, routing numbers ensure that transactions are processed accurately and efficiently.

Finding Your Routing Number

Locating your routing number is a simple process:

1. Check Your Checkbook

The routing number is typically printed at the bottom left corner of your checks. It appears as a series of nine digits and is usually followed by your account number and check number.

2. Online Banking

Most banks provide your routing number through their online banking portals. Log in to your account and look for the "Account Information" or "Settings" section.

3. Contact Your Bank

If you're unable to find your routing number, contact your bank's customer service department for assistance.

Security and Privacy Concerns

While routing numbers are essential for banking transactions, they also pose potential security risks. If someone gains access to your routing number and account information, they may be able to initiate unauthorized transactions. To protect yourself:

- Keep your routing number and account information confidential

- Monitor your account activity regularly

- Enable two-factor authentication for online banking

By taking these precautions, you can help safeguard your financial information.

Common Questions About ABA vs Routing Numbers

1. Can I Use My Routing Number for International Transactions?

No, routing numbers are only used for domestic transactions within the United States. For international transactions, you will need to provide a SWIFT code or IBAN.

2. Is My Routing Number the Same for All Transactions?

Most banks use the same routing number for all transactions, but some institutions may have separate routing numbers for ACH and wire transfers. Check with your bank to confirm.

3. How Often Do Routing Numbers Change?

Routing numbers rarely change, but mergers or acquisitions may result in updates. Always verify your routing number with your bank if you suspect changes.

Conclusion

In conclusion, understanding the differences between ABA vs routing numbers is crucial for navigating the modern banking system. These nine-digit codes play a vital role in ensuring that your transactions are processed accurately and securely. By familiarizing yourself with the functions and applications of routing numbers, you can make informed decisions about your financial activities.

We encourage you to share this article with others who may benefit from the information. If you have any questions or comments, feel free to leave them below. Additionally, explore our other resources for more insights into banking and finance.

Data Sources: Federal Reserve, Accuity

{kind=link}