What Is An ABA Routing Number: A Comprehensive Guide To Understanding And Using It

ABA routing numbers play a crucial role in the banking system, acting as a unique identifier for financial institutions in the United States. These numbers ensure that funds are routed correctly between banks during transactions such as direct deposits, wire transfers, and check processing. Understanding what an ABA routing number is and how it works can help you manage your finances more effectively and avoid potential errors in banking processes.

The term "ABA routing number" refers to a nine-digit code assigned to banks and credit unions by the American Bankers Association (ABA). This code is essential for facilitating seamless transactions within the U.S. banking system. Whether you're setting up direct deposits, paying bills online, or transferring money between accounts, knowing your bank's ABA routing number is critical.

With the increasing reliance on digital banking and electronic transactions, the importance of ABA routing numbers has grown significantly. In this article, we will delve into the details of what an ABA routing number is, how it works, its various uses, and how you can find it. By the end, you'll have a thorough understanding of this essential banking tool.

Read also:How To Find The Right Ups Customer Support Number For Your Needs

Table of Contents:

- Overview of ABA Routing Numbers

- Structure of an ABA Routing Number

- Common Uses of ABA Routing Numbers

- How to Find Your ABA Routing Number

- ABA vs. SWIFT: Key Differences

- Security Concerns with ABA Routing Numbers

- A Brief History of ABA Routing Numbers

- Regulations and Standards

- Troubleshooting Common Issues

- Conclusion and Next Steps

Overview of ABA Routing Numbers

ABA routing numbers were first introduced in 1910 by the American Bankers Association as a way to streamline check processing. Since then, their role has expanded to include facilitating various types of financial transactions. Each bank or credit union in the United States is assigned one or more unique ABA routing numbers, depending on its size and operations.

These numbers are critical for ensuring that funds are transferred accurately and efficiently between financial institutions. Without them, the banking system would face significant challenges in processing transactions.

Why Are ABA Routing Numbers Important?

- They provide a standardized way to identify banks and credit unions.

- They help prevent errors in transactions by ensuring funds are routed to the correct institution.

- They enable the automation of banking processes, reducing the need for manual intervention.

Structure of an ABA Routing Number

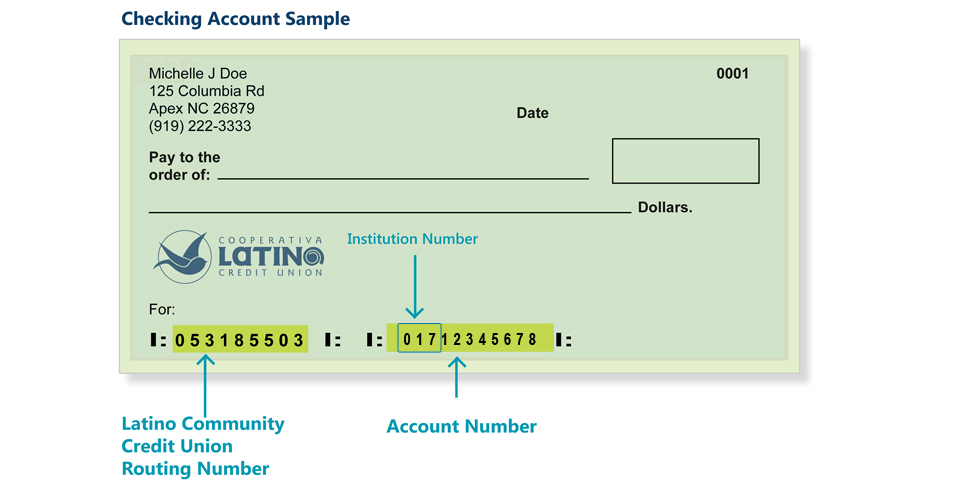

An ABA routing number consists of nine digits, each with a specific purpose. The structure is as follows:

- First four digits: Represent the Federal Reserve routing symbol.

- Fifth and sixth digits: Indicate the ABA institution identifier.

- Seventh digit: Identifies the Federal Reserve check processing center assigned to the bank.

- Eighth digit: Represents the Federal Reserve district where the bank is located.

- Ninth digit: Acts as a checksum digit to validate the routing number's accuracy.

How Does the Checksum Work?

The checksum digit is calculated using a mathematical formula that ensures the routing number is valid. This helps prevent errors and fraud by verifying the authenticity of the number.

Common Uses of ABA Routing Numbers

ABA routing numbers are used in a variety of financial transactions. Here are some of the most common uses:

Read also:Bay News 9 Radar Tampa Fl Your Ultimate Guide To Local Weather Updates

- Direct deposits: Employers use ABA routing numbers to deposit employees' salaries directly into their bank accounts.

- Bill payments: Customers can use ABA routing numbers to pay bills electronically.

- Wire transfers: These numbers are essential for sending and receiving funds domestically.

- Check processing: Routing numbers help banks identify the institution that issued a check.

Are ABA Routing Numbers Used Internationally?

ABA routing numbers are primarily used for domestic transactions within the United States. For international transactions, SWIFT codes are typically used instead.

How to Find Your ABA Routing Number

Finding your ABA routing number is relatively straightforward. Here are some common methods:

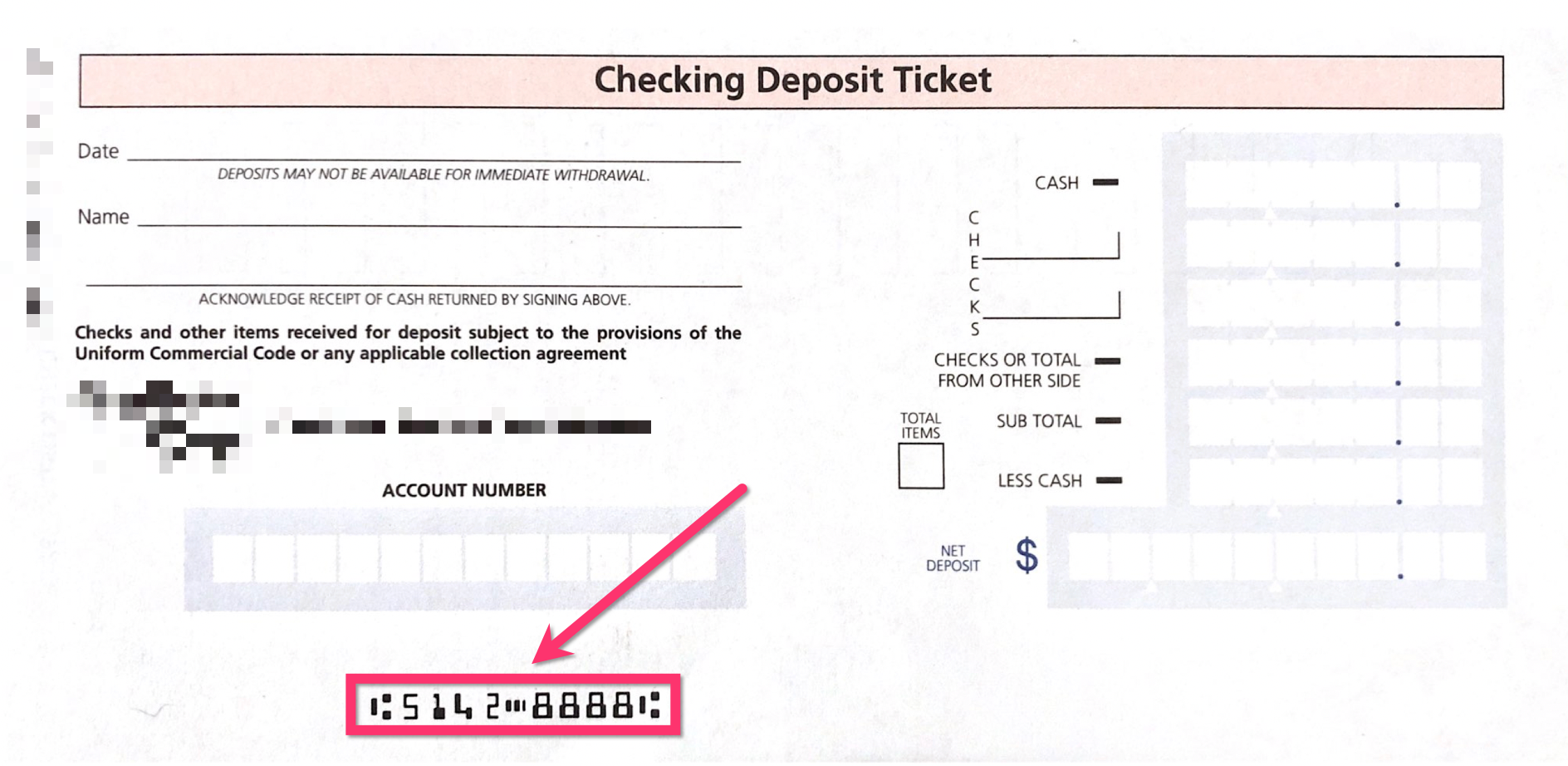

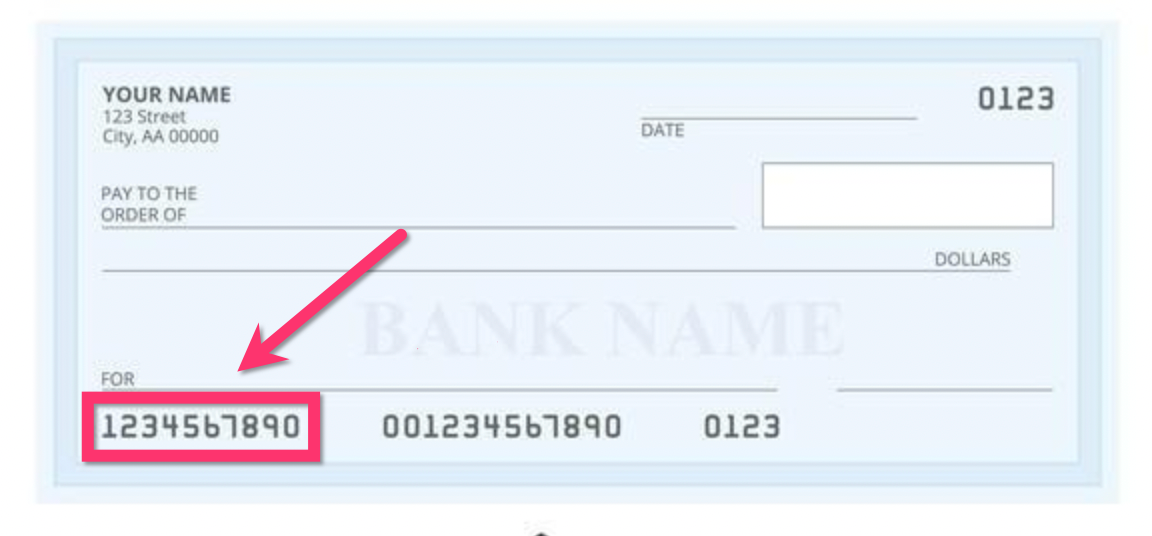

- Check the bottom of your checks: The routing number is usually the first set of numbers printed at the bottom left of your checks.

- Check your bank's website: Most banks provide routing numbers on their websites under account information or FAQs.

- Call your bank: Customer service representatives can provide your routing number over the phone.

Can You Have Multiple ABA Routing Numbers?

Yes, larger banks may have multiple ABA routing numbers depending on the state or region where you opened your account. Always confirm the correct number with your bank.

ABA vs. SWIFT: Key Differences

While ABA routing numbers are used for domestic transactions, SWIFT codes are used for international transactions. Here are some key differences:

- Scope: ABA routing numbers are domestic, while SWIFT codes are international.

- Length: ABA routing numbers are nine digits, while SWIFT codes are eight to eleven characters.

- Purpose: ABA routing numbers facilitate transactions within the U.S., while SWIFT codes enable global transfers.

Which One Should You Use?

Use an ABA routing number for domestic transactions and a SWIFT code for international transfers.

Security Concerns with ABA Routing Numbers

While ABA routing numbers are generally secure, there are some potential risks to be aware of:

- Fraud: Criminals may attempt to use stolen routing numbers to commit fraud.

- Human error: Incorrectly entering a routing number can lead to transaction errors.

To protect yourself, always verify the accuracy of your routing number before initiating a transaction.

How Can You Protect Your Routing Number?

Treat your ABA routing number like any other sensitive financial information. Avoid sharing it unnecessarily and keep your checks and account information secure.

A Brief History of ABA Routing Numbers

ABA routing numbers were first introduced in 1910 to standardize check processing. Over the years, their role has expanded to include facilitating electronic transactions. Today, they remain a vital component of the U.S. banking system.

How Have ABA Routing Numbers Evolved?

With the rise of digital banking, ABA routing numbers have become increasingly important for automating transactions. Advances in technology have also improved the security and accuracy of these numbers.

Regulations and Standards

ABA routing numbers are governed by strict regulations to ensure their accuracy and security. The American Bankers Association and the Federal Reserve work together to maintain these standards.

What Happens If a Routing Number is Incorrect?

If a routing number is incorrect, transactions may be delayed or returned. Always double-check the number before initiating a transaction.

Troubleshooting Common Issues

Here are some common issues you might encounter with ABA routing numbers and how to resolve them:

- Transaction errors: Verify the routing number and re-initiate the transaction.

- Delayed transactions: Contact your bank to confirm the routing number and check for processing delays.

When Should You Contact Your Bank?

If you're experiencing issues with your routing number, it's best to contact your bank for assistance. They can provide guidance and help resolve any problems.

Conclusion and Next Steps

ABA routing numbers are an essential component of the U.S. banking system, facilitating accurate and efficient transactions. By understanding what they are, how they work, and how to find them, you can better manage your finances and avoid potential errors.

We encourage you to explore further resources on banking and finance to deepen your knowledge. Don't hesitate to share this article with others who may find it helpful. For more insights and tips, check out our other articles on personal finance and banking.

References: