What Is Bank's ABA Number: A Comprehensive Guide To Understanding ABA Routing Numbers

In today's financial world, understanding the banking system and its terminologies is crucial, especially when it comes to transferring money. One of the essential components of the U.S. banking system is the ABA number. If you've ever wondered, "What is bank's ABA number?" this article will provide you with a detailed overview of ABA routing numbers, their importance, and how they function in various financial transactions.

Whether you're setting up direct deposits, initiating wire transfers, or paying bills online, the ABA number plays a vital role in ensuring your money reaches the right destination. This article will walk you through everything you need to know about ABA numbers, including their history, structure, and practical applications.

By the end of this guide, you'll have a clear understanding of what an ABA number is and how it impacts your banking activities. Let's dive in!

Read also:What Temperature Do You Cook Shrimp A Comprehensive Guide For Perfectly Cooked Shrimp

Table of Contents

- What is Bank's ABA Number?

- History of ABA Numbers

- Structure of an ABA Number

- Uses of ABA Numbers

- ABA Number vs. SWIFT Code

- How to Find Your Bank's ABA Number

- Security Concerns with ABA Numbers

- The Importance of ABA Numbers in Banking

- Challenges with ABA Numbers

- The Future of ABA Numbers

What is Bank's ABA Number?

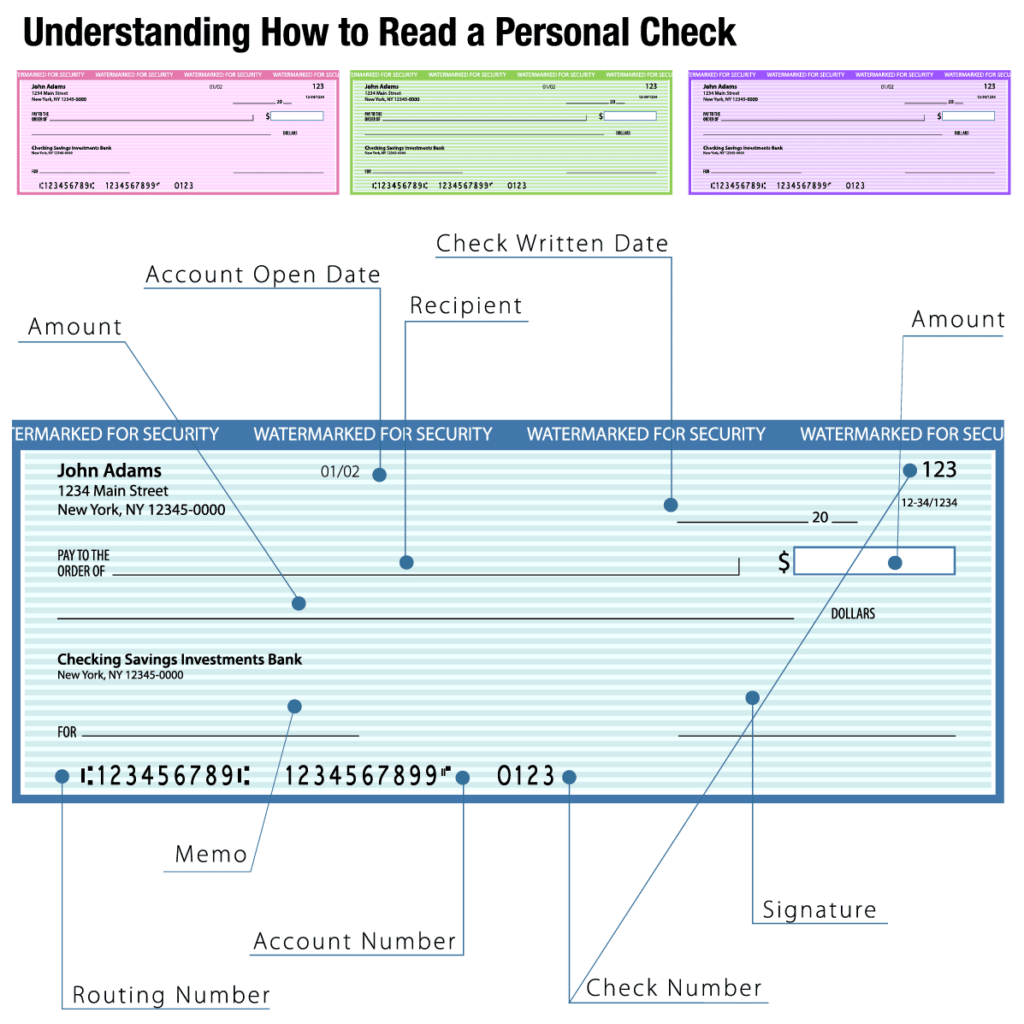

Bank's ABA number, also known as the American Bankers Association routing number, is a unique nine-digit code assigned to financial institutions in the United States. This number identifies the specific bank or credit union and is essential for processing financial transactions such as checks, direct deposits, and electronic funds transfers.

The ABA number ensures that your money is routed to the correct financial institution. Without it, banks wouldn't be able to verify the origin and destination of funds, leading to potential errors in transactions.

Why is the ABA Number Important?

Here are some reasons why the ABA number is crucial:

- Ensures accurate routing of funds

- Facilitates efficient processing of checks and electronic payments

- Reduces the risk of fraud and errors

History of ABA Numbers

The ABA routing number system was introduced in 1910 by the American Bankers Association to standardize check processing. Before the implementation of ABA numbers, there was no uniform way to identify banks, which often led to confusion and delays in transactions.

Today, the system is managed by Accuity, a provider of regulatory and financial crime compliance solutions. Accuity assigns and maintains ABA numbers, ensuring they remain up-to-date and accurate.

Structure of an ABA Number

An ABA number consists of nine digits, each with a specific purpose:

Read also:How Old Was Lynda Carter In Wonder Woman A Comprehensive Look At The Iconic Role

- Digits 1-4: Federal Reserve Routing Symbol

- Digits 5-8: Financial Institution Identifier

- Digit 9: Check Digit

The check digit is used to verify the accuracy of the ABA number. It ensures that the number is valid and correctly formatted.

How to Validate an ABA Number

To validate an ABA number, you can use the following formula:

(Digit 1 × 3) + (Digit 2 × 7) + (Digit 3 × 1) + (Digit 4 × 3) + (Digit 5 × 7) + (Digit 6 × 1) + (Digit 7 × 3) + (Digit 8 × 7) + (Digit 9 × 1) = A multiple of 10

If the result is a multiple of 10, the ABA number is valid.

Uses of ABA Numbers

ABA numbers are used in various financial transactions, including:

- Direct deposits

- Wire transfers

- Automated Clearing House (ACH) transactions

- Check processing

- Bill payments

Each of these transactions relies on the ABA number to ensure that funds are correctly routed to the intended recipient.

Direct Deposits

Direct deposits are one of the most common uses of ABA numbers. Employers use ABA numbers to deposit employees' salaries directly into their bank accounts, eliminating the need for paper checks.

ABA Number vs. SWIFT Code

While both ABA numbers and SWIFT codes are used for financial transactions, they serve different purposes. ABA numbers are used for domestic transactions within the United States, while SWIFT codes are used for international transactions.

Key differences between ABA numbers and SWIFT codes include:

- Length: ABA numbers are nine digits, while SWIFT codes are 8-11 characters.

- Purpose: ABA numbers are for domestic transactions, while SWIFT codes are for international transactions.

- Format: ABA numbers consist of digits only, while SWIFT codes include letters and numbers.

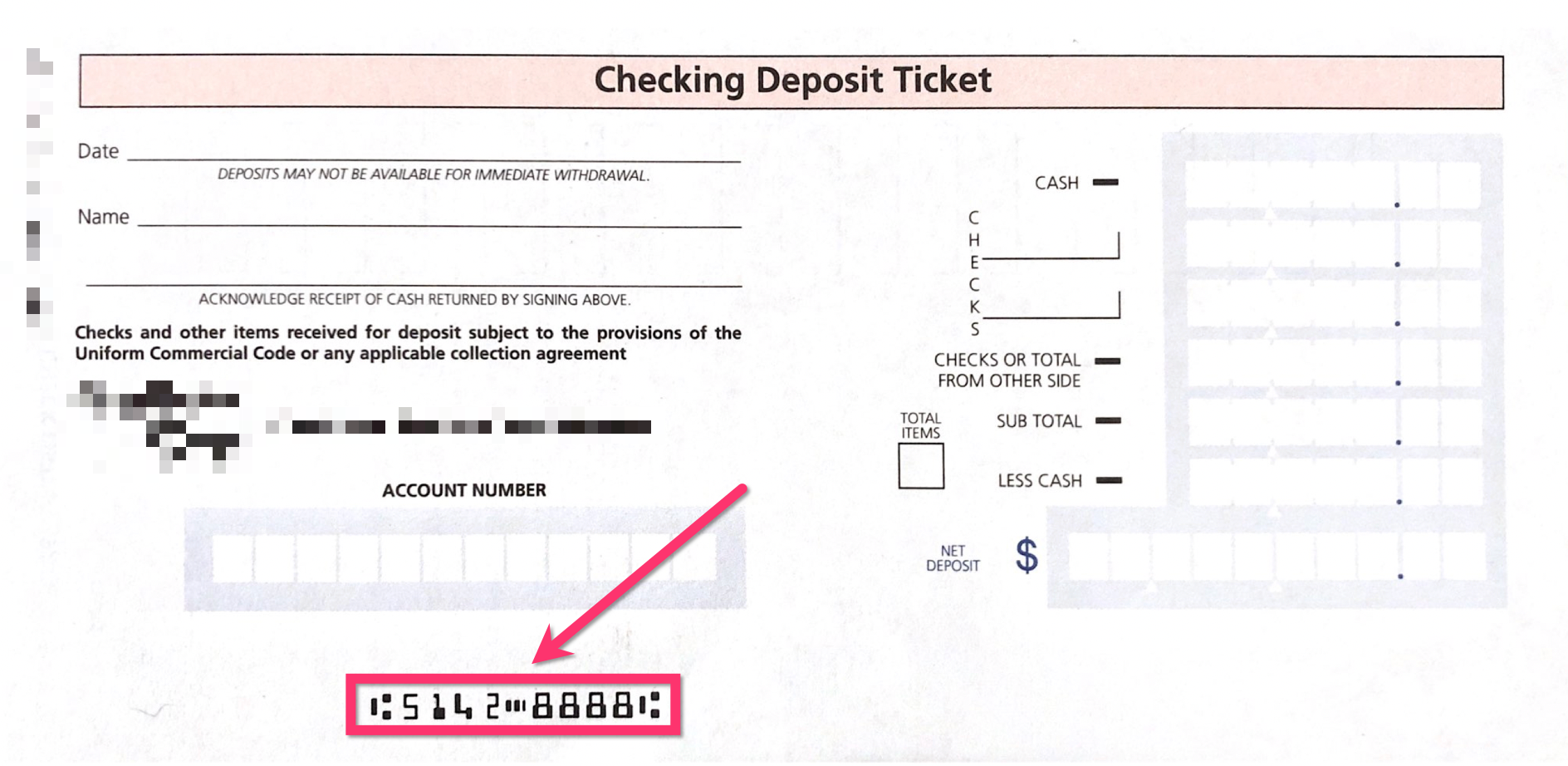

How to Find Your Bank's ABA Number

Finding your bank's ABA number is relatively simple. Here are a few methods:

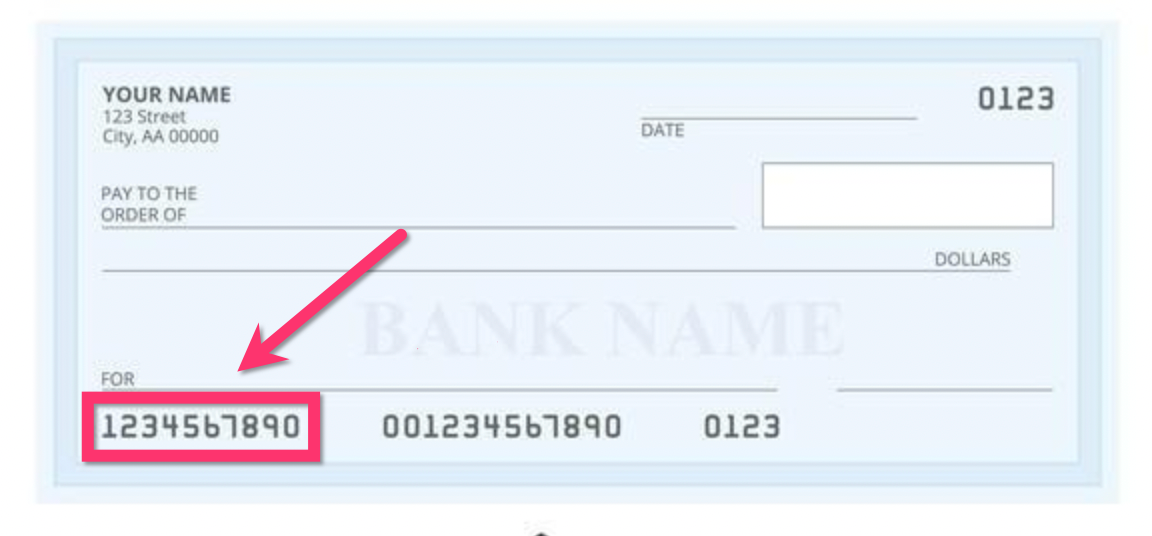

1. Check Your Checks

Look at the bottom of your checks. The ABA number is usually the first set of numbers printed there. It consists of nine digits and is typically located on the left side.

2. Contact Your Bank

Reach out to your bank's customer service department. They can provide you with the ABA number associated with your account.

3. Online Banking

Many banks display the ABA number in their online banking portals. Log in to your account and check the account information section.

Security Concerns with ABA Numbers

While ABA numbers are essential for financial transactions, they can also pose security risks if not handled properly. Sharing your ABA number with unauthorized parties can lead to fraudulent activities, such as unauthorized withdrawals or transfers.

To protect your ABA number:

- Only share it with trusted entities

- Monitor your account for suspicious activity

- Use secure methods to transmit your ABA number

The Importance of ABA Numbers in Banking

ABA numbers are a cornerstone of the U.S. banking system. They ensure that financial transactions are processed accurately and efficiently. Without ABA numbers, banks would struggle to identify accounts and route funds correctly.

Additionally, ABA numbers play a critical role in reducing fraud and errors. By providing a standardized method for identifying financial institutions, ABA numbers help maintain the integrity of the banking system.

Challenges with ABA Numbers

Despite their importance, ABA numbers are not without challenges. Some of the common issues include:

- Outdated System: The ABA routing number system was introduced over a century ago and may not be suited for modern banking needs.

- Security Risks: As mentioned earlier, sharing ABA numbers can lead to fraudulent activities.

- Confusion: Some banks have multiple ABA numbers for different types of transactions, which can cause confusion for customers.

The Future of ABA Numbers

As technology continues to evolve, the role of ABA numbers in banking may change. While they remain a vital component of the U.S. banking system, there is growing interest in exploring alternative systems that offer greater security and efficiency.

For example, blockchain technology and digital identifiers could potentially replace traditional ABA numbers in the future. These innovations promise to enhance the speed, security, and accuracy of financial transactions.

Conclusion

In conclusion, understanding what bank's ABA number is and how it works is essential for anyone engaging in financial transactions. From direct deposits to wire transfers, ABA numbers ensure that your money is routed correctly and securely.

As we move toward a more digital and interconnected financial system, the importance of ABA numbers will likely evolve. However, for now, they remain a critical component of the U.S. banking infrastructure.

We encourage you to take action by:

- Checking your ABA number for accuracy

- Sharing this article with others who may benefit from the information

- Exploring other articles on our site for more insights into the world of finance

Stay informed and secure in your financial dealings!

Sources

2. Accuity

3. American Bankers Association