What Is ABA Number: A Comprehensive Guide To Understanding The ABA Routing Number System

Understanding the ABA number is essential for anyone who deals with banking transactions in the United States. Whether you're setting up direct deposits, initiating wire transfers, or issuing checks, knowing what an ABA number is and how it functions can streamline your financial processes. In this article, we'll delve into the intricacies of the ABA routing number system, its history, and its relevance in modern banking.

ABA numbers, also known as routing transit numbers (RTNs), play a crucial role in the U.S. banking system. They ensure that funds are directed to the correct financial institution, making transactions more efficient and secure. As you navigate through this guide, you'll gain a deeper understanding of how these numbers work and their significance in various banking activities.

This article is designed to provide valuable insights into the ABA number system, addressing key questions such as "What is an ABA number?" and "How do you find your ABA number?" By the end of this guide, you'll have a clear understanding of the ABA routing number system and its importance in facilitating seamless financial transactions.

Read also:Five Finger Death Punch Over And Under A Comprehensive Guide

Table of Contents

- What is an ABA Number?

- History of the ABA Routing Number

- Purpose of ABA Numbers

Structure of an ABA Number

- Importance of ABA Numbers in Banking

- Common Uses of ABA Numbers

- How to Find Your ABA Number

- ABA Numbers vs. SWIFT Codes

- Security Concerns with ABA Numbers

- The Future of ABA Numbers

What is an ABA Number?

An ABA number, or routing transit number (RTN), is a nine-digit code used by banks and other financial institutions in the United States to identify themselves in financial transactions. This number ensures that funds are routed to the correct bank or credit union during transfers, checks, or automated clearing house (ACH) transactions.

The ABA number is crucial for domestic transactions within the U.S. and is widely used for processes such as direct deposits, bill payments, and wire transfers. It acts as a digital address for financial institutions, enabling seamless communication between banks.

History of the ABA Routing Number

The ABA routing number system was introduced in 1910 by the American Bankers Association (ABA) to facilitate check processing. Before the introduction of this system, banks faced challenges in identifying the origin of checks, leading to delays and errors in transactions.

Over the years, the ABA number system has evolved to accommodate advancements in technology and the increasing complexity of financial transactions. Today, it remains a cornerstone of the U.S. banking infrastructure, ensuring accurate and efficient fund transfers.

Purpose of ABA Numbers

The primary purpose of ABA numbers is to ensure that financial transactions are routed to the correct institution. They serve as a unique identifier for banks and credit unions, enabling the smooth processing of checks, electronic payments, and other financial activities.

ABA numbers are also used in various banking operations, including:

Read also:Dan And Phil Merch A Comprehensive Guide For Fans

- Direct deposits

- Bill payments

- Wire transfers

- Automated Clearing House (ACH) transactions

Structure of an ABA Number

An ABA number consists of nine digits, each serving a specific purpose. The structure is as follows:

- First four digits: Represent the Federal Reserve Routing Symbol.

- Next four digits: Identify the financial institution.

- Ninth digit: Acts as a checksum digit to verify the validity of the ABA number.

This structure ensures that each ABA number is unique and can be easily validated using a checksum algorithm.

Importance of ABA Numbers in Banking

ABA numbers play a vital role in the U.S. banking system by ensuring the accuracy and security of financial transactions. They help prevent errors in fund transfers, reducing the risk of fraud and financial losses.

Furthermore, ABA numbers enable banks to process transactions efficiently, saving time and resources for both institutions and customers. Their importance extends to various aspects of banking, including:

- Facilitating domestic transactions

- Ensuring secure fund transfers

- Streamlining banking operations

Common Uses of ABA Numbers

ABA numbers are widely used in various banking activities, including:

- Direct deposits: Employers use ABA numbers to deposit salaries directly into employees' bank accounts.

- Bill payments: Customers can use ABA numbers to pay bills electronically, avoiding the need for physical checks.

- Wire transfers: ABA numbers are essential for domestic wire transfers, ensuring funds are sent to the correct bank.

- ACH transactions: These electronic transfers rely on ABA numbers to process payments between banks.

Understanding the uses of ABA numbers can help individuals and businesses optimize their financial operations.

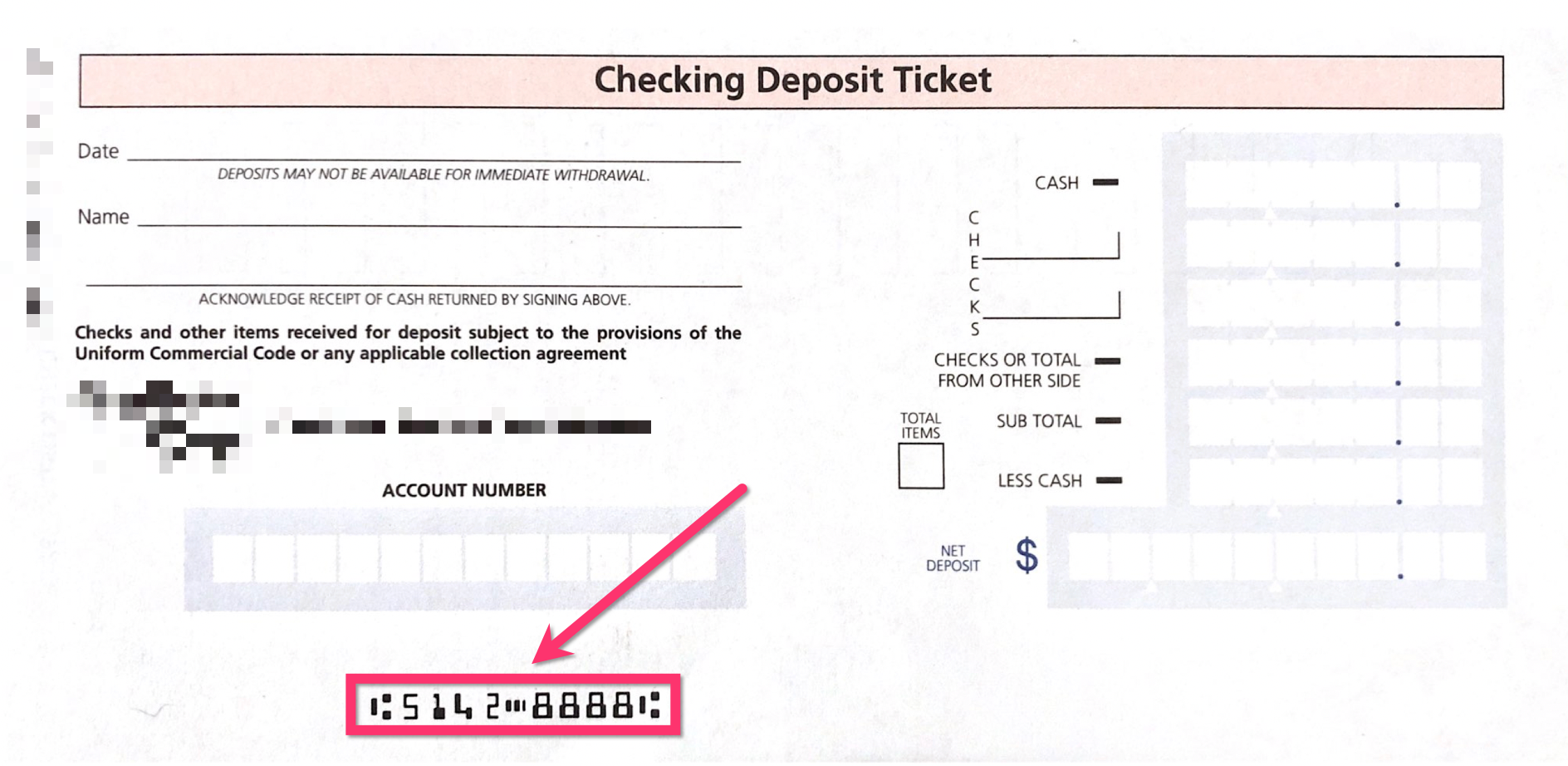

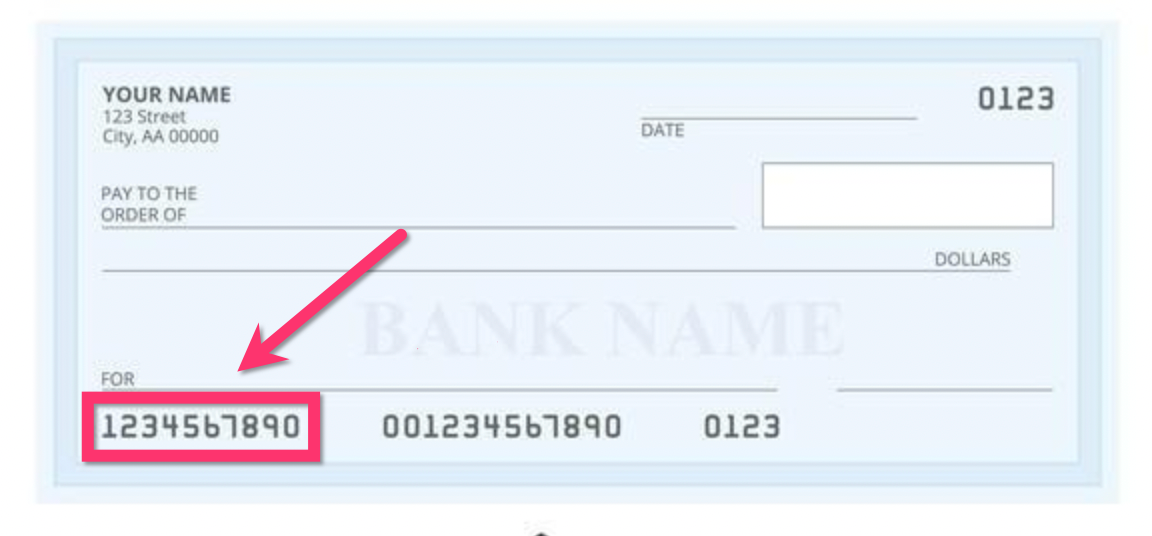

How to Find Your ABA Number

Finding your ABA number is a straightforward process. You can locate it in several ways:

- Checkbook: The ABA number is typically printed on the bottom left corner of your checks.

- Bank statement: Your bank statement may include the ABA number for reference.

- Online banking: Most banks provide ABA numbers through their online banking platforms.

- Customer service: Contact your bank's customer service for assistance in locating your ABA number.

Having access to your ABA number is essential for conducting various banking transactions.

ABA Numbers vs. SWIFT Codes

While ABA numbers and SWIFT codes both serve to identify financial institutions, they differ in their scope and application:

- ABA numbers: Used for domestic transactions within the United States.

- SWIFT codes: Facilitate international transactions between banks worldwide.

Understanding the distinction between these two systems is crucial for individuals and businesses engaged in global financial activities.

Security Concerns with ABA Numbers

Although ABA numbers are designed to enhance the security of financial transactions, they are not immune to misuse. Fraudsters may attempt to exploit ABA numbers for unauthorized transactions, highlighting the need for vigilance.

To protect your ABA number and safeguard your financial information:

- Keep your ABA number confidential and avoid sharing it unnecessarily.

- Monitor your bank account regularly for suspicious activity.

- Use secure methods for transmitting ABA numbers, such as encrypted email or secure online platforms.

By adopting these practices, you can minimize the risk of fraud and ensure the security of your financial transactions.

The Future of ABA Numbers

As technology continues to evolve, the role of ABA numbers in the banking system is likely to expand. Innovations in digital banking and financial technology (fintech) may lead to new applications for ABA numbers, enhancing their functionality and relevance.

Despite these advancements, the fundamental purpose of ABA numbers—to ensure accurate and secure financial transactions—will remain unchanged. Their importance in the U.S. banking system is expected to persist, underscoring the need for continued education and awareness about their use and security.

Conclusion

In conclusion, understanding what an ABA number is and its role in the U.S. banking system is crucial for anyone involved in financial transactions. From facilitating direct deposits to ensuring secure fund transfers, ABA numbers play a vital role in modern banking.

We encourage you to explore further resources and stay informed about the latest developments in financial technology. If you have any questions or insights to share, feel free to leave a comment below. Additionally, consider sharing this article with others who may benefit from learning about ABA numbers and their significance in banking.

Data Source: Federal Reserve | American Bankers Association

{kind=link}